Blockchain is a decentralized and distributed digital ledger technology that records transactions across many computers in a way that the registered transactions cannot be altered retroactively.

- Decentralization: Unlike traditional databases that are typically controlled by a central authority, a blockchain is maintained by a network of nodes (computers) that collaborate to validate and record transactions.

- Transparency: All transactions recorded on a blockchain are visible to all participants in the network. This transparency can help reduce fraud and increase trust among users.

- Immutability: Once a transaction is recorded on a blockchain, it is very difficult to change or delete it. This is achieved through cryptographic hashes, which securely link blocks of data together.

- Consensus Mechanisms: Blockchains use different methods to achieve agreement among network participants about the validity of transactions. Common consensus mechanisms include Proof of Work (PoW), Proof of Stake (PoS), and others.

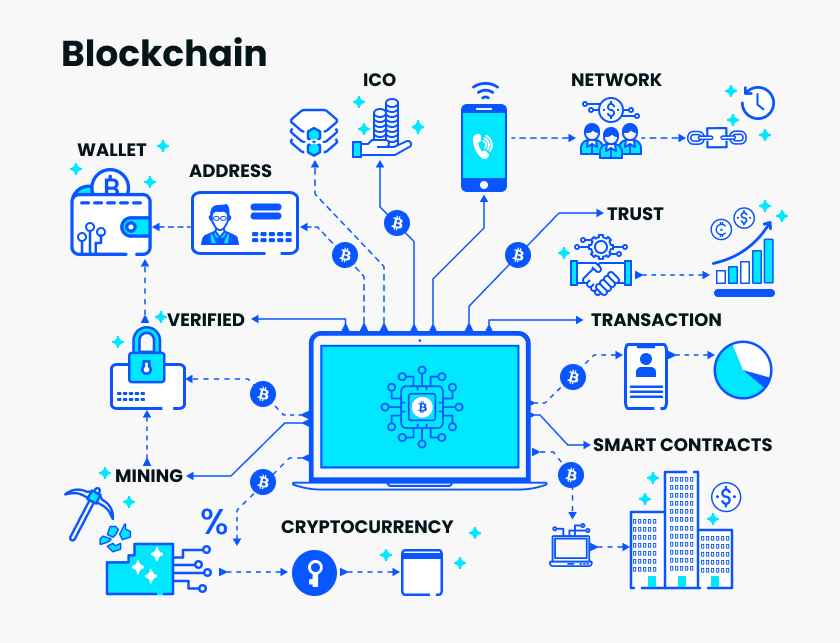

- Smart Contracts: These are self-executing contracts with the terms of the agreement directly written into code. They automatically execute actions based on predefined conditions, facilitating and enforcing contracts without intermediaries.

- Use Cases: Beyond cryptocurrencies, blockchain can be applied in various fields:

- Supply Chain Management: Enhancing transparency and traceability in the logistics of goods.

- Healthcare: Securely storing patient records and ensuring data integrity.

- Voting Systems: Creating tamper-proof voting systems to enhance electoral transparency.

- Financial Services: Streamlining cross-border transactions and reducing fraud.

- Public vs. Private Blockchains: Public blockchains (like Bitcoin) are open to anyone and fully decentralized, while private blockchains are restricted to certain entities and are often used by businesses for internal processes.

- Tokens and Cryptocurrencies: Many blockchains have their own native cryptocurrencies (like Ether for Ethereum) and may also support various tokens that represent assets or utility within the ecosystem.

Understanding blockchain technology can provide insights into how it could reshape industries and improve various processes through enhanced security, transparency, and efficiency. If you have specific questions or need more details on a particular aspect of blockchain, feel free to ask!

Comments are closed